The Tadawul All Share Index closed at 10,830.73 on Monday amid a volatile regime, with 20-day momentum at –4.90 and a market-wide average RSI of 34.91 — firmly in oversold territory. Breadth favored advancers decisively: 183 stocks rose against 72 decliners with none unchanged. The divergence at the sector level was stark, however — of 22 sectors, only 4 advanced, 17 declined, and 1 was flat, suggesting heavyweight names bore the brunt of selling while smaller constituents edged higher.

Banks led the large-cap declines, falling 2.86% despite internal breadth of 8 advancers to 2 decliners. Materials shed 2.19% on 76.2 million shares, yet showed broad-based underlying strength with 37 stocks advancing versus just 6 declining; the 30-day Materials-Brent correlation stands at –0.13. Energy was the session's bright spot among major groups, rising 0.67% with 6 advancers and 1 decliner. Financial Services was the weakest sector at –3.37%, followed by Transportation at –3.34% and Consumer Services at –3.29%.

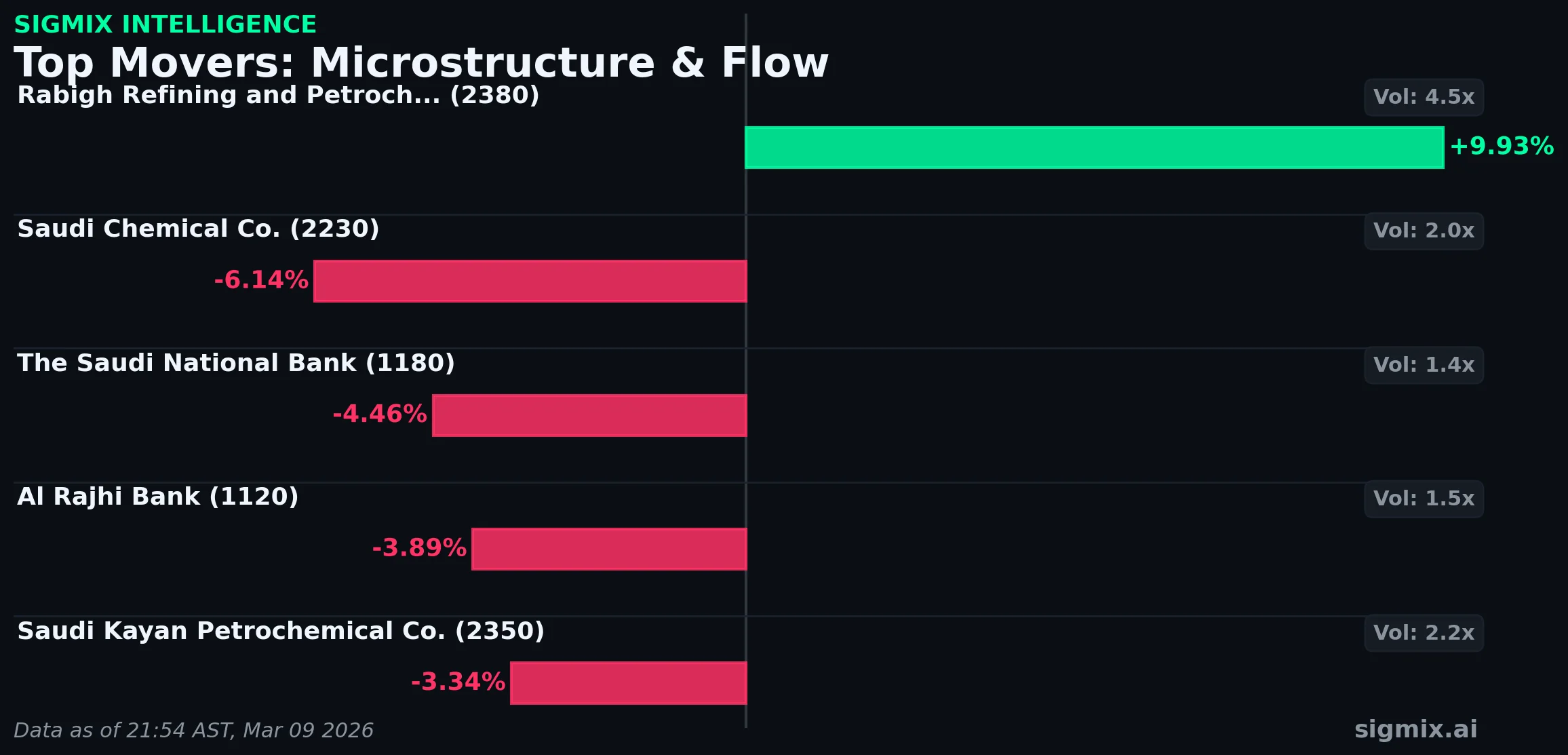

Rabigh Refining and Petrochemical Co. (2380) surged 9.93% to SAR 9.41 on 23.9 million shares, trading at 4.50x its 20-day average volume. Smart money flow was detected alongside buying pressure and an elevated large order ratio of 37.94, with the liquidity indicator registering a strongly positive reading. The refiner's trailing P/E is negative at –2.55, reflecting ongoing operational losses. Rabigh does not currently have earnings or analyst coverage in the dataset. Saudi Arabian Oil Co. (2222) gained 0.67% to SAR 27.12 on 31.2 million shares at 2.08x average volume. The liquidity indicator pointed to buying pressure with an order imbalance of 1.59 and active market maker participation. Aramco trades at a trailing P/E of 17.09 with a forward P/E of 15.45; 16 analysts project consensus EPS of SAR 1.56 with high disagreement. On the earnings front, Aramco has a 50% historical beat rate with its most recent quarter a beat.

Al Rajhi Bank (1120) declined 3.89% to SAR 98.80 on 6.3 million shares at 1.51x average volume. Institutional selling and selling pressure were both flagged, accompanied by volume-price divergence. The bank trades at a trailing P/E of 17.57 with a price-to-book of 3.58. Al Rajhi has beaten estimates in 6 consecutive quarters, though its longer-term beat rate stands at 44%. The TLT-Al Rajhi transmission channel remains strong at a 30-day correlation of 0.37. Saudi Kayan Petrochemical Co. (2350) dropped 3.34% to SAR 5.21 on 24.9 million shares at 2.16x average volume. The liquidity indicator pointed to selling pressure with institutional selling flagged and volume-price divergence observed. Saudi Kayan trades at a negative trailing P/E of –3.93 and has a historical beat rate of just 19%, though its most recent quarter was a beat.

Saudi Chemical Co. (2230) was the session's sharpest decliner among the most-active names, falling 6.14% to SAR 7.18 on 13.7 million shares at 1.96x average volume. Institutional selling and selling pressure were both flagged alongside volume-price divergence, with the liquidity indicator pointing to selling pressure. The stock trades at a trailing P/E of 21.06. The Saudi National Bank (1180) fell 4.46% to SAR 39.02 on 8.0 million shares at 1.40x average volume. Institutional selling was active with selling pressure flagged and volume-price divergence present. SNB trades at a trailing P/E of 9.97 and has a 95% historical beat rate, though its most recent quarter was a miss.

"According to the Sigmix Microstructure Engine: Rabigh Refining (2380) recorded net order flow of +4,430 with an order flow ratio of 0.648, while Saudi Kayan (2350) registered net outflow of –19,273 with an order flow ratio of –0.361 and institutional selling active — capturing sharp divergence in institutional conviction across the petrochemical-energy complex on a day when Brent surged over 10%."

Brent crude surged 10.72% to $104.21, yet the XLE-Aramco channel remains broken at –0.27 correlation, deteriorating by 0.19 over the past week. The USO-Aramco channel is weak at –0.27 correlation. Gold eased 1.22% to $5,106.98. The US equity regime is neutral for 10 consecutive days. The SPY-TASI channel holds at normal status with 0.13 correlation and a seven-day delta of +0.03, indicating limited direct transmission from US equities into the Saudi market.

Q4 GDP growth (YoY final) is scheduled for today, with consensus at 4.9% versus a prior reading of 4.8%. Industrial Production YoY for January is due March 10. February inflation data — CPI YoY, MoM, and wholesale prices — is scheduled for March 15.

What is not confirmed: Whether Brent's 10.7% single-session surge will sustain or reverse, altering energy-sector momentum. Whether the broken XLE-Aramco correlation will re-couple given the oil price spike. Whether the disconnect between positive stock-level breadth (72% advancing) and negative sector-level breadth (17 of 22 declining) reflects rotation or an index-weighting effect. Whether the market-wide oversold RSI of 34.91 will prompt institutional re-entry in coming sessions.

This report is produced by the Sigmix Intelligence Desk for informational purposes only. It does not constitute investment advice, a recommendation, or an offer to buy or sell any security. Past performance and microstructure signals are not indicative of future results. Investors should conduct their own due diligence and consult a licensed financial advisor before making investment decisions.