The Saudi equity market ended its Sunday session under a bear regime, with 20-day momentum at –9.06% and the market-wide average RSI at 27.85—firmly in oversold territory. Annualised 20-day volatility stood at 32.4%. Individual stock breadth diverged sharply from the sector-level picture: 183 names advanced against 72 decliners with none unchanged. At the sector level, however, only 2 of 22 sectors closed higher while 20 retreated, pointing to large-cap-weighted declines in heavyweight groups.

Banks led the broad decline, falling 3.64% on volume of 41.1 million shares; sector breadth was 8 advancing against 2 declining, suggesting the sell-off was concentrated in large-cap constituents rather than a uniform rout. Materials shed 2.41% despite markedly positive breadth of 37 advancers to 6 decliners—again indicating index-weight drag. The 30-day materials–Brent correlation stood at –0.13, reflecting limited direct oil price transmission into the petrochemical complex. Energy was the session's clear outlier, rallying 3.13% with breadth of 6 advancing to 1 declining, buoyed by the crude rally. Software and Services was the weakest sector, falling 7.35%.

Saudi Arabian Oil Co. (2222) closed at SAR 25.80, up 3.37%, on volume running at 1.95x its 20-day average. The stock trades at a trailing P/E of 16.53 and a forward P/E of 14.95, with a 252-day beta of 0.61. Aramco's most recent quarterly earnings were a beat, with 3 consecutive beats and a historical beat rate of 50.0% over reported quarters. Sixteen analysts cover the name with a consensus EPS estimate of SAR 1.56 for fiscal 2026, though analyst disagreement is rated high.

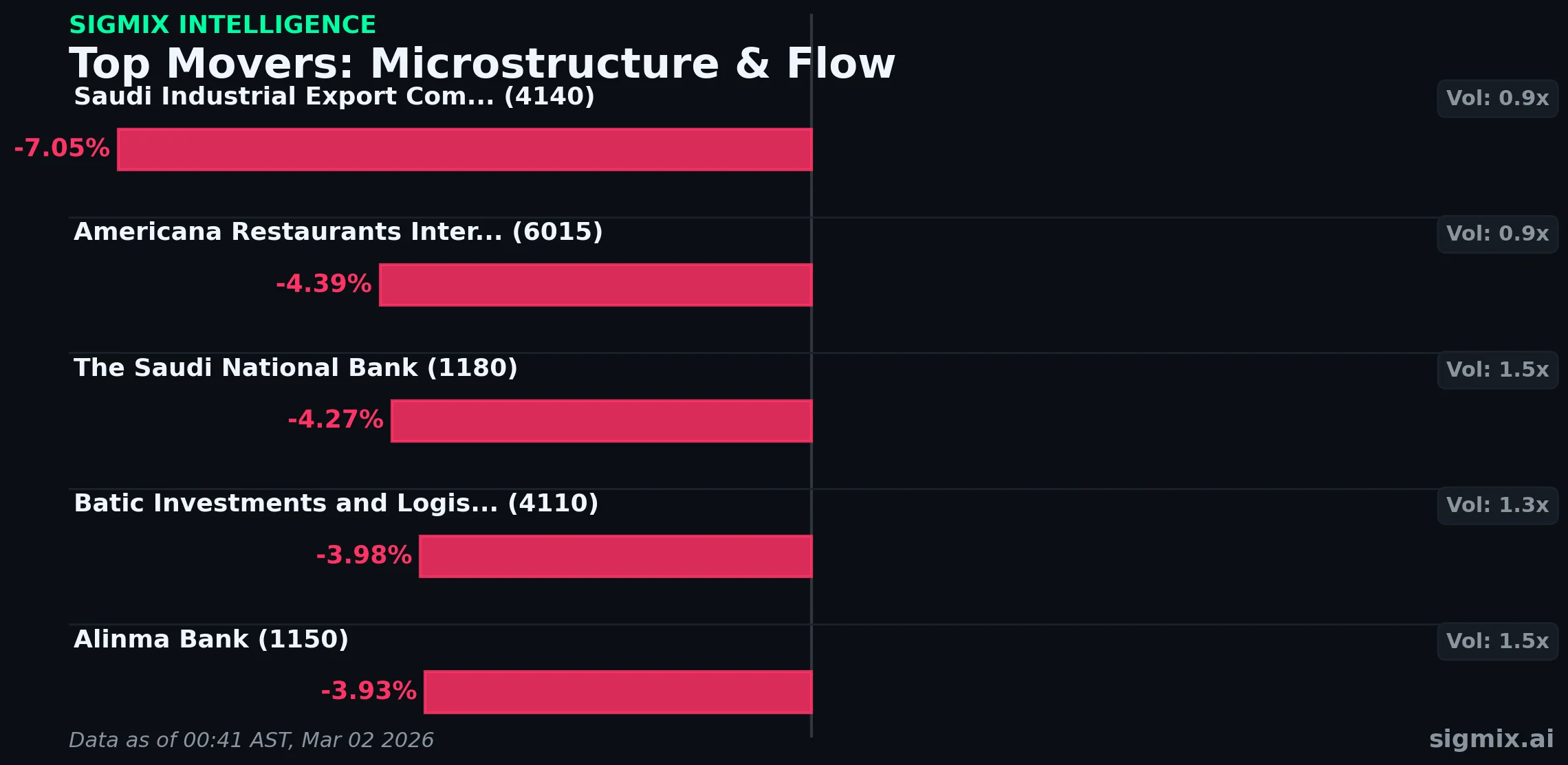

Al Rajhi Bank (1120) fell 3.42% to SAR 97.55 on volume of 1.72x average, driving its 14-day RSI to 13.82. The lender carries a trailing P/E of 17.27 and a 252-day beta of 1.12. Its most recent quarter was a beat, extending a streak of 6 consecutive beats, though the longer-term beat rate stands at 44.4%. The Saudi National Bank (1180) declined 4.27% to SAR 39.90 on 1.51x average volume with an RSI of 23.10. SNB trades at a trailing P/E of 10.34 and a price-to-book of 1.33; its longer-term earnings beat rate is 95.0% over 20 quarters, though the most recent result was a miss.

Saudi Kayan Petrochemical Co. (2350) slipped 2.29% to SAR 4.70 on volume of 0.89x average—below its 20-day norm. The petrochemical producer carries a negative trailing P/E of –3.93, reflecting ongoing losses, though its most recent quarter was a beat and its recent 4-quarter beat rate is 50.0%. Saudi Industrial Export Co. (4140) posted the steepest single-stock decline among the session's notable movers, falling 7.05% to SAR 2.24 on volume of 0.95x average with an RSI of 24.19 and a 252-day beta of 0.96. Americana Restaurants (6015) fell 4.39% to SAR 1.96 on volume of 0.92x average despite an RSI of 73.91 that still reflects an uptrend; its most recent quarter was a beat. Alinma Bank (1150) declined 3.93% to SAR 26.88 on 1.50x average volume, with an RSI of 36.29 and a trailing P/E of 11.81; its most recent quarter was a miss.

"The Sigmix Quantitative Engine notes that microstructure analytics for this Sunday session are unavailable due to stale upstream data. Readers are directed to sigmix.ai for the latest data when refreshed on the next trading day."

Brent crude surged 2.87% to $72.87, extending its year-to-date gain to 19.30%. Gold advanced 1.79% to $5,278.32, up 20.72% for the year. The U.S. regime shifted to neutral two days ago from risk-on. The SPY-TASI correlation channel reads 0.05 at normal status with a delta of –0.025 over seven days, while the XLE-Aramco channel stands at 0.24 with weak status—limiting cross-market transmission.

No corporate events or economic data releases are currently scheduled on the near-term calendar. Market participants should monitor the persistence of deeply oversold RSI readings across the banking sector alongside the continuation of the bear regime for signs of mean-reversion or further downside momentum.

What is not confirmed:

- Whether the divergence between positive individual stock breadth (183 advancers) and negative sector breadth (20 of 22 declining) reflects genuine rotation or temporary large-cap rebalancing.

- Whether oversold RSI readings in banks—Al Rajhi at 13.82 and SNB at 23.10—will trigger a technical bounce or signal further downside.

- Whether Brent's 2.87% rally will transmit to the broader Saudi market given the weak 21-day TASI–Brent correlation of 0.21.

This report is produced by the Sigmix Intelligence Desk for informational purposes only. It does not constitute investment advice, a recommendation, or an offer to buy or sell any security. All data is derived from automated quantitative models and may contain errors. Past performance is not indicative of future results. Readers should consult a licensed financial advisor before making investment decisions. Sigmix is not licensed by the Saudi Capital Market Authority.